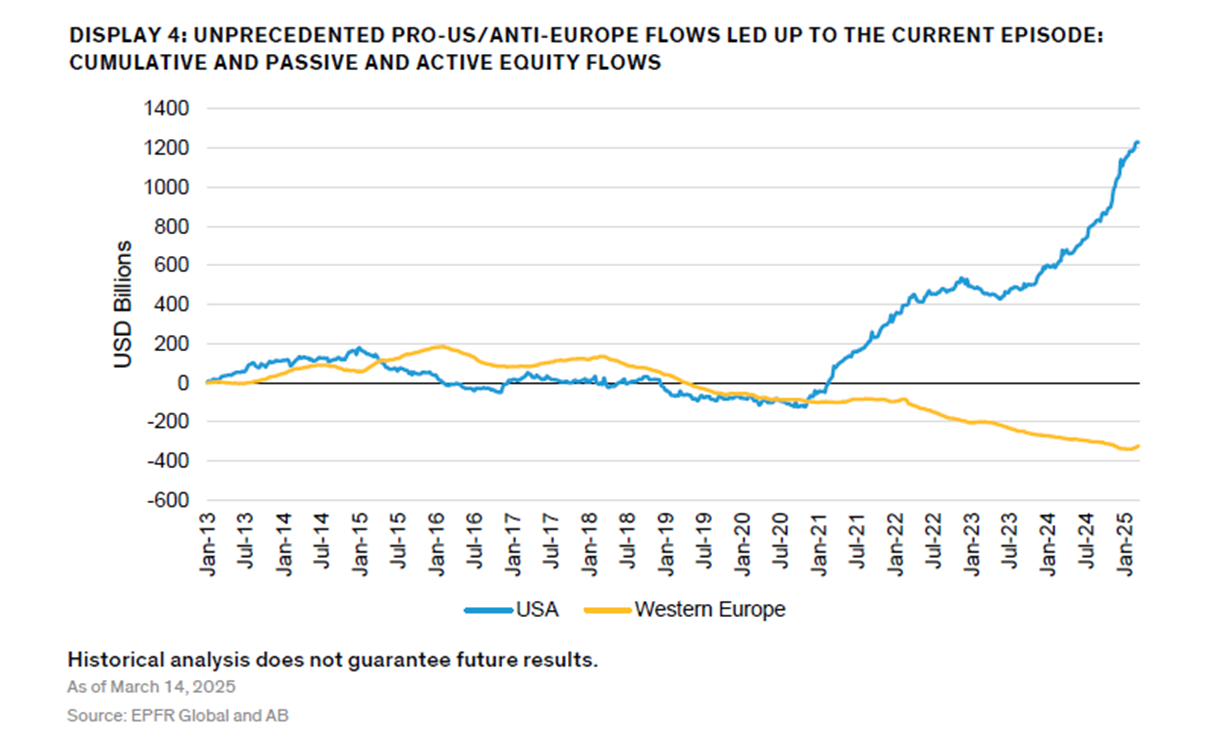

Three things here ...

Adversarial geo-economic policies make it harder to keep pushing for over allocation to US assets and ... at the same time ...the world has gotten itself over allocated to US assets ... so if the appetite to keep re-buying into that position shifts (even if its moves slowly and incrementally as it has in China) it would have a effect at the margin for asset prices, perhaps not in the US (as there is a huge domestic capital market that is hyper efficient across almost all dimensions of risk) but moreover in markets like Europe where risk capital has been less free flowing and doesnt always find its way to the parts of the market that need it...The interesting piece for Europe will be the degree to which US capital decides to front run any shift - if the US market decides that Europe is the place to be for the next 3 or 4 years this would accelerate the upcoming capital allocation cycle ... and in our asset class being ahead of those flows is always the path to better risk adjusted returns.